Buying Out a Former Partner’s Undivided Share of the Family Home

The following five key points should be carefully observed:

1. Determining the Value of the Property

The valuation of the property is the starting point for all calculations, and in particular for determining the amount of the equalisation payment (soulte) to be made. Obtaining at least three valuations from an expert or a notary enables the couple to select the mean or median of the values proposed, depending on the extent of the divergence between the estimates.

2. Verifying the Matrimonial or Civil Partnership Regime

The ownership share in the property depends primarily on the matrimonial property regime, the civil partnership (PACS) regime, or the regime applicable to cohabiting couples. Many couples mistakenly believe that ownership shares depend solely on each party’s contribution to the repayment of the mortgage loan.

- For spouses married under the statutory or contractual community of property regime, or partners under a PACS entered into before 1 January 2007 without opting for the separation of property regime: irrespective of whether one party financed the greater part of the property, the ownership share is 50/50.

- For spouses married under a separation of property contract, or partners under a PACS entered into after 1 January 2007 subject to the separation of property regime: each party’s respective contribution is taken into account.

This latter situation may give rise to disputes and require judicial intervention. Evidence as to the origin of payments made will need to be produced.

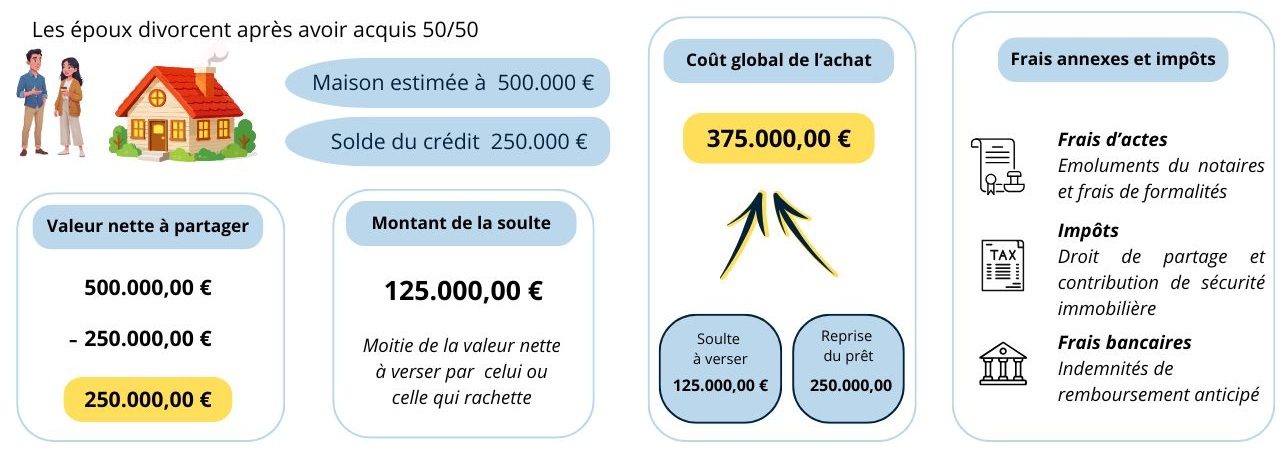

3. Calculating the Equalisation Payment

Depending on whether a mortgage loan is outstanding, the equalisation payment (soulte) may vary.

The calculation is performed on the basis of the agreed valuation, less the outstanding capital remaining on the mortgage loan. The outstanding loan balance is obtained by consulting the mortgage amortisation schedule.

The resulting figure, after deduction of the outstanding loan amount, is then divided in accordance with each party’s ownership share, as determined by the applicable matrimonial or civil partnership regime.

4. Assessing the Additional Costs

In addition to the equalisation payment, various ancillary costs must be factored in. In most cases, the buyout will involve taking out a new mortgage loan to discharge the existing joint loan. Early repayment charges are frequently levied by the lender or bank and must therefore be anticipated.

Partition costs must also be budgeted for. The partition duty (droit de partage) amounts to 1.1% of the value of the property for married or PACS couples, and 2.5% for cohabiting couples. These costs are increased by land registry formality fees and notarial remuneration.

5. Retaining the Existing Mortgage Loan

Where the interest rate on the loan taken out by the couple is particularly favourable in comparison with current market rates, the buying-out party has an interest in retaining it.

To do so, they must submit a request to their lender or bank, which may refuse if the borrower’s income is deemed insufficient. If the request is granted, they may apply for the release of the other spouse or partner and their removal from joint and several liability for the repayment instalments.

In the event of a refusal to retain the existing loan, the acquiring spouse or partner will be required to discharge the outstanding loan and take out a new mortgage in their own name.